NOTE: This is a repost from the Department of Education’s Official Blog

On Aug. 8, 2020, President Trump extended the 0% student loan interest rate and suspension of payments on federal student loans owned by the Department of Education (ED) until Dec. 31, 2020. These relief measures began March 13, 2020.

If you’re considering or already participating in Public Service Loan Forgiveness (PSLF) or Temporary Expanded Public Service Loan Forgiveness (TEPSLF), you may have questions about how this suspension of payments or other Coronavirus-related changes will impact your progress.

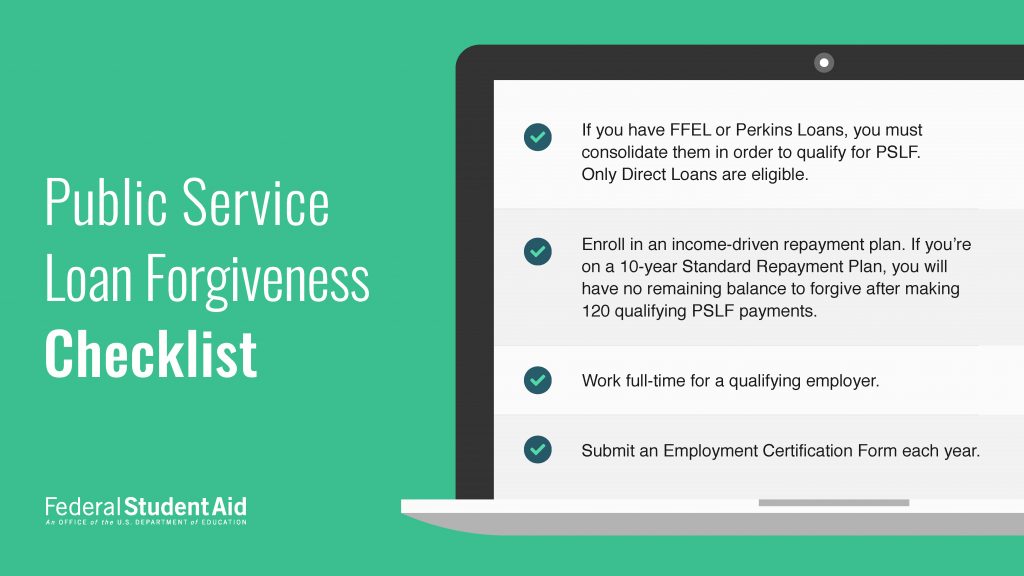

Before we look at those impacts, here’s a checklist of basic tips for PSLF.

{kind=link}

1. Suspended Monthly Payments

If you

- have Direct Loans that are not in default, and

- work full-time for a qualifying employer during the extension of the suspension of payment period,

suspended monthly payments will count toward Public Service Loan Forgiveness (PSLF) as if you continued to make regular monthly payments. You can think of them as $0 payments. You’ll need to submit an Employment Certification Form to receive credit for your employment during the suspension of payments. Borrowers with in-grace, in-school, and certain deferment, forbearance, and bankruptcy statuses are not eligible for credit toward PSLF. The Higher Education Relief Opportunities for Students (HEROES) Act of 2003 provides authority for this action.

Temporary Expanded Public Service Loan Forgiveness (TEPSLF)

Similarly, you will receive payment credit during the suspension of payments as if you had made real payments—as long as all other TEPSLF qualifications are met. This includes ensuring that both the amount you paid 12 months prior to applying for TEPSLF and the last payment you made before applying for TEPSLF were at least as much as you would have paid under an income-driven repayment (IDR) plan. To confirm your required monthly payment for TEPSLF, contact FedLoan Servicing.

Refunds

If you made a payment between March 13, 2020, and the end of the payment suspension period, and would like a refund, the payment still counts toward PSLF as long as all other PSLF qualifications are met.

Applying for PSLF

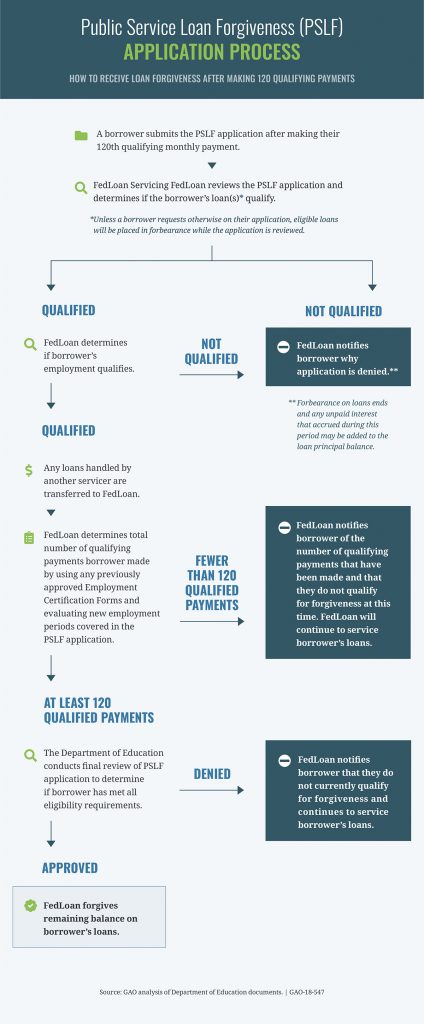

If you reach your 120 qualifying payments during the payment suspension period, you can still apply for and receive PSLF at this time. However, you must be working for a qualifying employer at the time you submit the PSLF application and at the time the remaining balance on your loan is forgiven. If you are eligible for forgiveness, the amount forgiven will be the principal and interest that was due after you made your 120 qualifying payments.

{kind=link}

{kind=link}

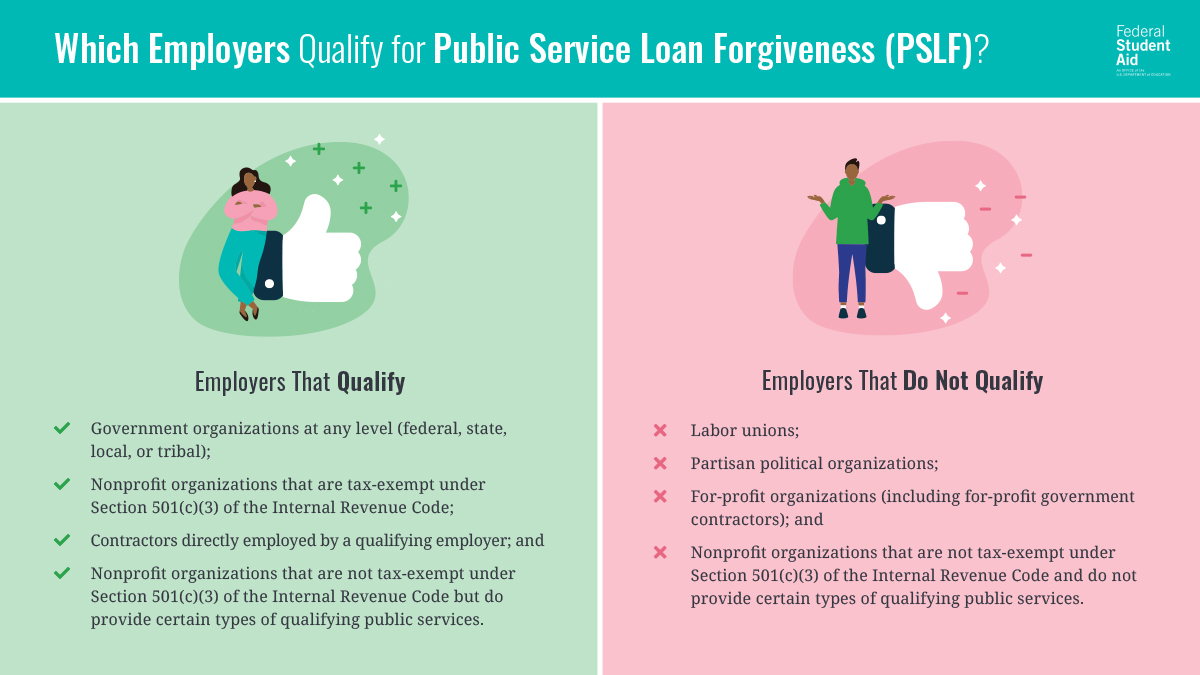

2. Reduced Work Hours Could Impact Your Eligibility

You must continue to work full-time (30 hours or more per week) for a qualifying employer to have the suspended payments count toward PSLF. You can meet the full-time requirement by being employed part-time for multiple employers, but they must all be qualifying employers.

{kind=link}

If you no longer work full-time for a qualifying employer, the suspended payments from the time you went below 30 hours per week or lost your employment (or were laid off or furloughed) will not count toward PSLF. You don’t lose your eligibility for PSLF entirely. If you later meet the qualifying employer and full-time status requirements, payments you make at that point will count toward PSLF and can be added to the count of qualifying payments you had when you originally went below 30 hours per week or lost your employment with a qualifying employer.

3. Additional Payments Will Reduce Your Amount Forgiven

In most cases, it’s a good financial strategy to make additional payments, if you can, during the 0% interest period. If you are seeking PSLF, however, additional payments may not be in your best interest.

If you make payments during the period of suspended payments, they won’t make you eligible for PSLF sooner. The suspended $0 payments already qualify toward your required 120 PSLF payments, so not making additional payments maximizes the amount to be forgiven.

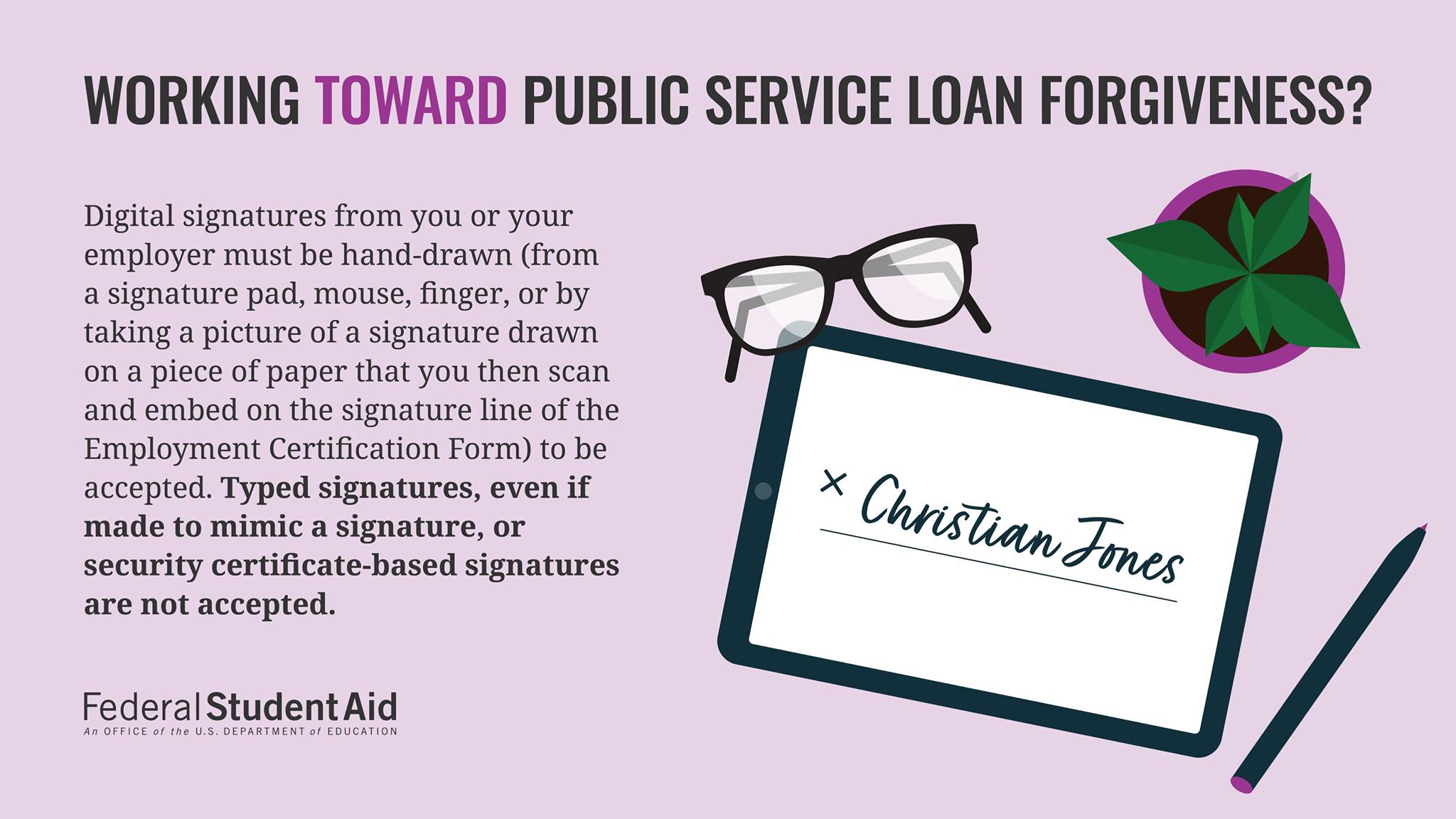

4. Receiving Credit During the Payment Suspension

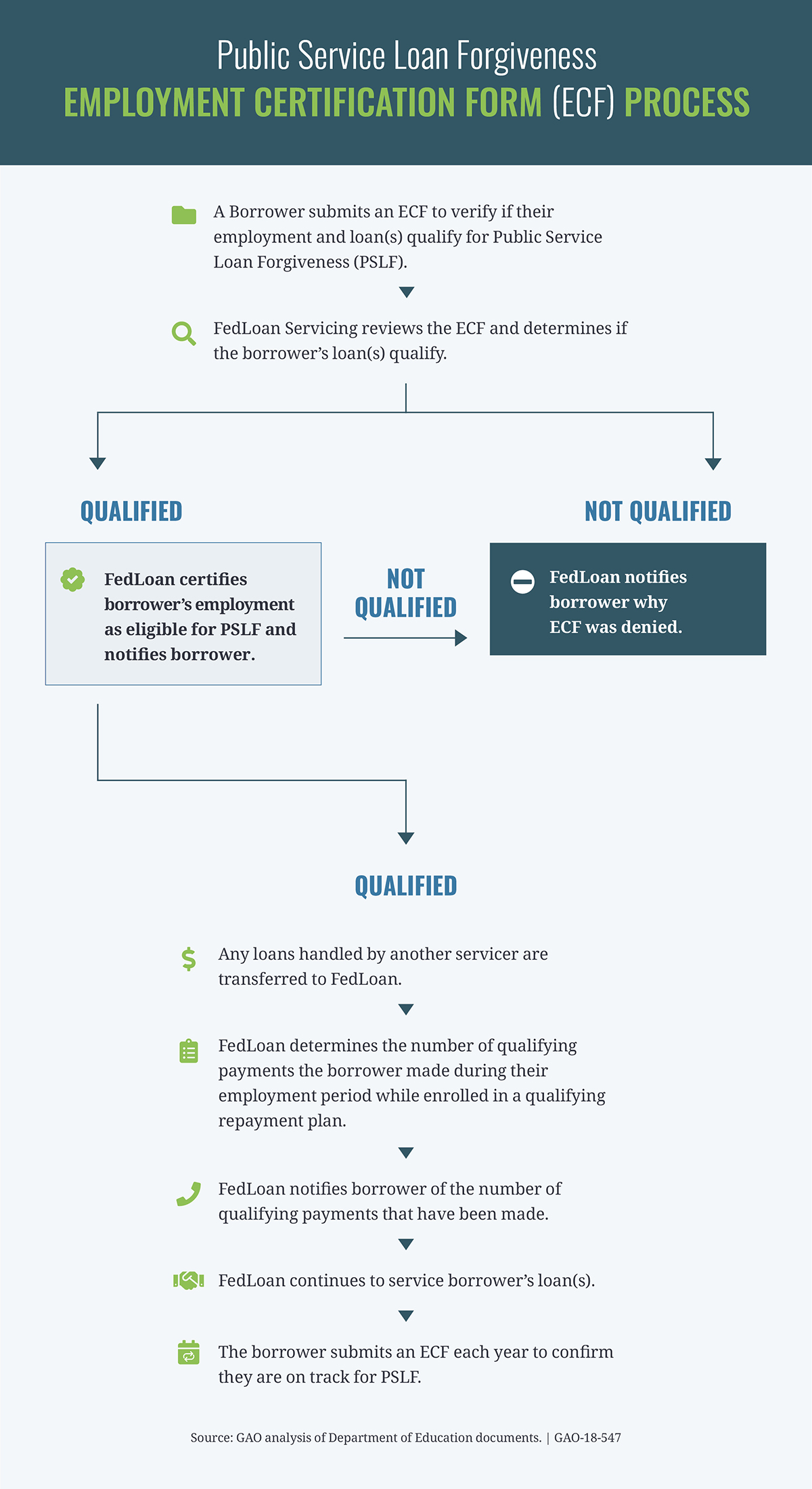

As a reminder, the best way to confirm you are meeting PSLF requirements is to submit your Employment Certification Form (ECF). Use the PSLF Help Tool to generate a prefilled ECF. Print it, sign it, have your employer sign it, and submit it to FedLoan Servicing. Keep these signature requirements below in mind before submitting your ECF.

{kind=link}

Note: When you visit the FedLoan Servicing website, the timeline for reaching the number of qualifying payments for PSLF may appear to have been extended. This is only temporary. Your estimated eligibility date for forgiveness will be corrected.

5. Mark Your Calendar for Your IDR Plan Recertification Deadline

It’s important to recertify on time, so that you remain on your IDR plan. If you aren’t on an IDR plan, payments you make after the payment suspension period ends won’t count toward PSLF. If your repayment plan recertification fell between March 13, 2020 to Sept. 30, 2020, your recertification date has now been pushed out six months from your original recertification date. Consider the following example:

- If your recertification date is May 12, 2020, your new recertification date will be Nov. 12, 2020.

Your loan servicer will notify you when it is time to recertify your plan. Wrong contact info means you’ll be missing important updates about your federal student loans. Log in now to confirm your info is correct. Be on the lookout for this email or letter to ensure you don’t miss your IDR recertification deadline.

{kind=link}

6. Remember to Avoid PSLF Scams!

There is no fee for the suspension of payments and other federal student loan benefits—not from the federal government and not from your loan servicer. If someone asks for money to suspend payments on your loans or help you apply for PSLF (for example), it’s a scam. Learn more about avoiding student aid scams.

If you’re looking for more general tips on how to apply for PSLF successfully, check out Applying for Public Service Loan Forgiveness: 5 Tips for Success or watch the video below.

_________________

This article was written by Miranda H., a Digital Engagement Strategist at the U.S. Department of Education’s office of Federal Student Aid.

Disclaimer: This article contains general statements of policy under the Administrative Procedure Act issued to advise the public on how ED and Federal Student Aid (FSA) propose to exercise their discretion as a result of and in response to the lawfully and duly declared COVID-19. ED and FSA do not intend for this article to create legally binding standards to determine any member of the public’s legal rights and obligations for which noncompliance may form an independent basis for action